Systemic Risk and Indian Financial Market

Here we give materials relating to the financial networks project that Sheri Markose and Simone Giansante were involved in from 2011-2015 for the Reserve Bank of India. We digitally mapped the Indian financial system using bilateral who -whom liabilities data for financial institutions in India including core Indian banks, foreign banks, mutual funds, insurance companies and the Urban and Rural Cooperative banks. Within 12 months of digitally mapping the balance sheet linkages, we identified a potential Northern Rock situation about 2012 using our bespoke network centrality measures.

I. The Handbook and documentation for the financial network software we built called RBI Systemic Risk App, SRA for short, is given here.

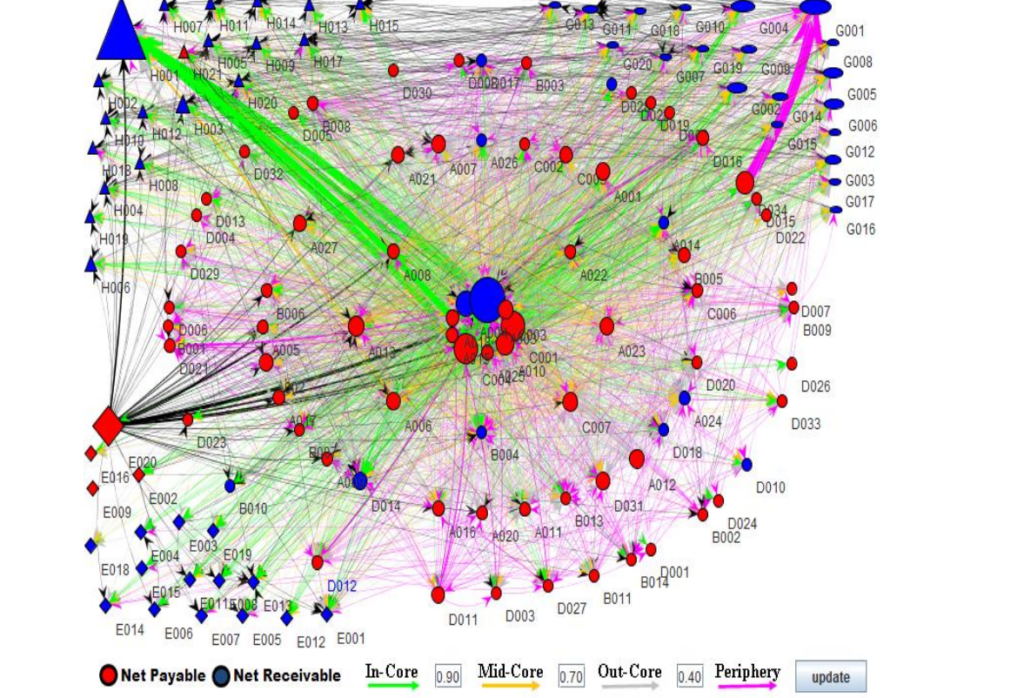

The famous graphic here for the Indian Financial system shows (1) Mutual Funds and Insurance Companies are net liquidity providers to Indian banks (2) A foreign bank can be seen borrowing heavily from and Indian mutual fund (3) A urban cooperative bank is a major borrower from rural cooperative banks indicating a vulnerability which led to problems

II. This RBI Network App is used for a number of papers and the executable of the RBI App Lite is given here

See Eurozone Cross border banking systemic risk paper. Who- whom balance sheet data is essential to avoid the misleading statistics for system risk that is used in mainstream finance based on market price based VaR, Co-Var etc.

Early warning of systemic risk in global banking: eigen-pair R number for financial contagion and market price-based methodsF

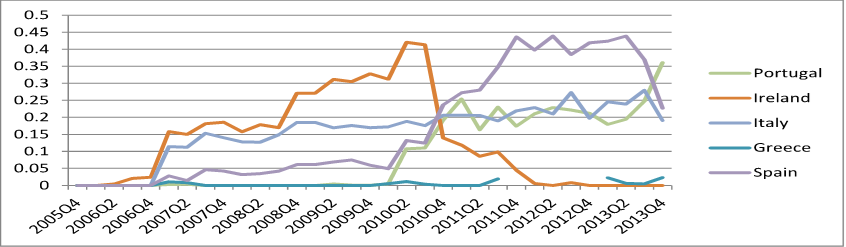

Specifically, for the PIIGS (Portugal, Ireland, Italy, Greece and Spain) of Eurozone area, what is remarkable is that the recent vulnerability of the Portugese banking system (light green) can clearly be seen in late 2013using the vulnerability index based on the Markose et. al. left eigenvector centrality metric. This eventually culminated in the collapse of the major Portugese Banco EspiritoSanto in August 2014, sparking fears of a second round of banking contagion in the Eurozone. The status of Portugal can be seen from the bottom panel of Figure 5 where by the end of 2013 Q4, Portugal becomes the most vulnerable banking system in the Eurozone.This was not anticipated by other methods of analysis such as those given by the IMF.

The Financial Times report on 10 August 2014 stated: In contrast with Ireland and Spain, banks were not seen as Portugal’s central vulnerability when it agreed to a €78bn bailout by the EU and the International Monetary Fund in 2011. In a progress report on the rescue in January, the IMF said “the financial sector remains stable” thanks to capital increases in the previous two years, while “adequate provisioning levels are being safeguarded through periodical impairment reviews”.

A systemic risk assessment of OTC derivatives reforms and skin-in-the-game for CCPs

III. The executable JAVA program for the RBI SRA App lite can be accessed below

Please follow document on how to upload the bilateral matrix data (csv files) and to run SRA App:

Put link to the Zip folder here